The Liability Regime for Non-Executive and Independent Directors in India: A Case for Reform

An examination of the current legal framework demonstrates the need to create safeguards for non-executive and independent directors.

Summary: The Report underscores the challenges present in the current legal framework governing the liability of non-executive and independent directors and presents informed recommendations to make the extant regime more efficient.

Introduction

In the aftermath of recent corporate scams (both in India and globally), the enforcement intensity against directors has increased significantly. While such intensity is necessary for discouraging wrongful conduct, caution must be exercised to ensure that it does not have unintended consequences.

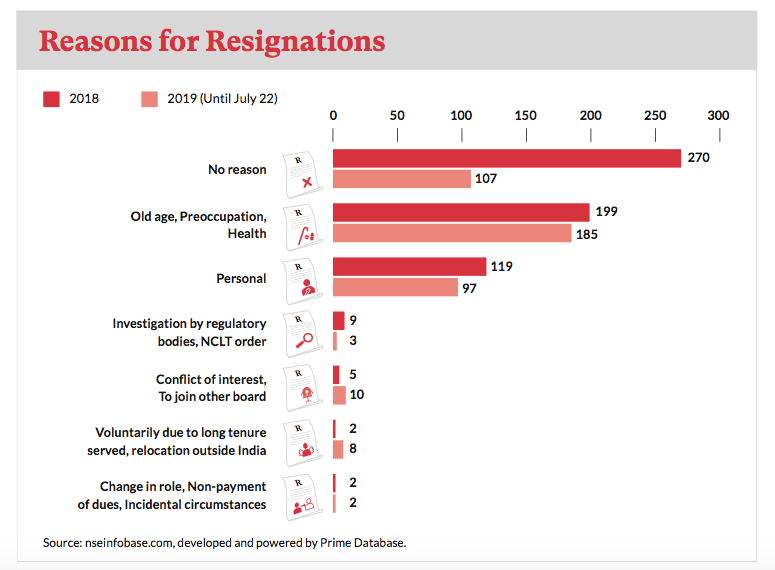

Data indicates that in India, the rate of resignation of independent directors from the boards of listed companies has increased significantly when compared to previous years (see figure below). Given the importance of qualified and upright independent directors for the development of our capital markets, this seems alarming.

Independent directors perform functions that are critical to good corporate governance, but the liability-related risks that such directors face seem disproportionate to their role. Some of these issues are relevant for other categories of non-executive directors as well.

Based on information available on nseinfobase.com, developed and powered by Prime Database (n. 14). Errors in interpreting the data, if any, are ours.

Even though the Companies Act provides for certain safe harbours, specifically for independent and non-executive directors with the objective of limiting their liability, it does not provide any safeguards at the stage where summons are issued to such directors by enforcement/investigating agencies.

To add to the issue, there are a host of other statutes that provide for offences attributable to companies and directors which have no specific safe harbours for independent and non-executive directors. As a result, such directors face significant risks not just in terms of liability but also reputational harm for acts that are beyond their control.

A report published by the Vidhi Centre for Legal Policy ‘The Liability Regime for Non-Executive and Independent Directors in India: A Case for Reform’ underscores the challenges present in the current legal framework governing the liability of non-executive and independent directors and presents informed recommendations.

Challenges in the current legal and regulatory framework

Limitations of safe harbours in Section 149(12) of the Companies Act: Independent directors and non-executive directors may be implicated not only for errors but also for passive negligence.

Lack of safe harbours in other statutes: A range of statutes governing various offences such as money laundering, tax evasion, securities frauds and environmental degradation do not recognise the distinction between executive and non-executive directors in their attribution of liability provisions. They do not provide for any safe harbours for independent and non-executive directors.

Factors impeding independence of independent directors: The processes relating to the appointment, removal and payment of remuneration of independent directors contribute to compromising their ‘independence’. This results in independent directors not being in a position to discharge their duties effectively.

Limitations of summoning provisions: In practice, notices are often sent to all directors. However, procedures that require taking into account the difference between notices and summons are not observed. Moreover, the safeguards provided under Section 149(2) of the Companies Act kick in only after investigative/legal proceedings have been initiated, resulting in substantial loss of reputation and harassment and inconvenience caused to independent and non-executive directors.

Fragmented enforcement regime: Multiple investigative/enforcement agencies deal with economic offences and there is no uniformity in procedures followed for conducting investigations and prosecutions.

Key recommendations

Enable a more ‘independent’ outside director model: The appointment process for independent directors should be made more stringent by limiting controlling shareholders’ influence in the process and by making their appointment subject to approval by non-controlling shareholders.

Harmonise the liability framework for directors across statutes: The liability framework for directors across all statutes recognising corporate offences should be harmonised with the Companies Act. This can be done by providing for the concept of ‘officer who is in default’ and enabling non-executive and independent directors to claim the protections designed specifically for them under the Companies Act.

Formulation and implementation of specific guidelines for investigating agencies/authorities: The procedures followed by investigating agencies/authorities for conducting investigations in relation to offences by companies must recognise the importance of creating safeguards for independent and non-executive directors. To this end, the formulation of guidelines to be followed by all investigating agencies/authorities specifically with respect to investigating offences by companies must be ensured. A permanent co-ordination committee (with representatives from all major investigation and prosecution agencies) should be set up for overseeing the implementation of such guidelines.

Issuance of summons: Summons should be issued to independent and non-executive directors only on arriving at the conclusion that there is a prima facie case against them based on a proper examination of the material and evidence on record. For a specified category of independent directors, a requirement may be imposed that they should not be summoned without prior authorisation from the co-ordination committee (referred to above) or a court of appropriate jurisdiction.

Introduce shareholder-sanctioned safe harbours for civil liability: Where civil liability is concerned, the viability of introducing shareholder-sanctioned safe harbours such as exculpatory clauses and statutorily recognising the business judgment rule as a defence should be examined.

Filed Under

About the Authors

Debanshu is one of Vidhi’s Co-Founders. He has over a decade of experience in commercial laws and the financial sector and has advised the Government of India on several legislative projects in this space. He was instrumental in advising the Government on the design and drafting of the Insolvency and Bankruptcy Code and its subsequent implementation. He has developed and curated Vidhi’s work on insolvency law, corporate law, financial regulation, and competition law and conceptualized its Bankruptcy Research Program. He has served as a member of a Government-appointed committee for operationalizing the National Company Law Tribunal and deposed before two Parliamentary committees examining financial sector legislation. He has also worked as a teaching fellow at Harvard Law School. He is an alumnus of the Harvard Law School, the University of Oxford, and Hidayatullah National Law University. He attended Harvard as a Fulbright Scholar and was awarded the Irving Oberman Memorial Prize in Bankruptcy and the Dean’s scholar prize in Corporations. He was also awarded a Distinction for his graduate studies at Oxford. In 2017, he was selected for NYU School of Law’s Hauser Global Scholarship, which he waived. His academic work has been published in peer-reviewed journals and an edited book published by Cambridge University Press, New York. He has been consulted by and mentioned in global business publications, such as IFR Asia and The Economist. Earlier, Debanshu practiced as an M&A and regulatory lawyer with AZB & Partners at its Mumbai and New Delhi offices.

Astha was a Senior Resident Fellow working in the area of Corporate Law and Financial Regulation. She completed her B.A.,LL.B. (Hons.) from the NALSAR University of Law in 2014 and her LL.M from the University of Cambridge in 2015.