Financial Inclusion of Women during the Pandemic

The Role of Jan Dhan accounts and Cash Transfers

Context

Financial inclusion has been consistently identified as one of the major drivers for the economic empowerment of women. Women are vulnerable to job loss and income loss and this was exacerbated during the pandemic, which deepened their financial exclusion.

In India, the pandemic witnessed women being disproportionately affected in terms of loss of economic opportunities. Existing literature indicates that as of 2021, the gender gap in terms of economic participation in the country worsened by 3%. It has also been estimated that, compared to 7% of men who lost their job, 47% of women lost their job permanently and did not return to the workforce at the end of 2020.

To mitigate the gendered impact of the pandemic, the Central Government introduced one of the largest cash transfers programmes under the flagship Pradhan Mantri Garib Kalyan Yojana (‘PMGKY’) initiative for women holding Pradhan Mantri Jan Dhan Yojana (‘PMJDY’) accounts. The objective of this programme was to enable women to maintain control over their finances and access financial services independently, to further their financial inclusion.

Assessing the impact of PMGKY cash transfers and use of financial services by women during the pandemic

Vidhi conducted a Study (‘Study’) to assess the effect of cash transfers on the financial behaviour of women as well as the overall accessibility and use of financial services by women during the pandemic. It also examined the adoption of digital financial services by women and specifically the role played by financial institutions (public and private sector banks, small finance banks, and payments banks) (‘FIs’) and business correspondents (‘BCs’) who were agents providing doorstep banking facilities, in furthering the financial inclusion of women during the pandemic.

PMJDY accounts and cash transfers under the PMGKY

Under the PMGKY initiative, during April 2020 – June 2020, the Central Government transferred INR 1500 to women-held PMJDY accounts (INR 500 each for three months). PMJDY accounts were introduced in 2014 as part of the National Mission on Financial Inclusion as a basic savings bank deposit account that could be opened by anyone who did not have any other bank account. It was one of the largest drives to ensure financial inclusion for socio-economically vulnerable communities and low-income groups and for the unbanked population so that they could have access to and could use formal finance channels. The PMJDY scheme has a national coverage of almost 45.57 crores beneficiaries, out of which 55% are women beneficiaries.

Conducting surveys

The Study relied on a combination of primary research as well as secondary literature where authors prepared questionnaires to collect data from 3 sets of respondents: 560 women customers, 17 BCs and 23 FIs.

The survey was conducted between March 2022 and May 2022. For women customers, the data collected on issues relating particularly to the PMGKY cash transfers pertained specifically to the months during which such cash transfers were made i.e., April 2020 – June 2020.

Districts for the survey were selected based on the Crisil Inclusix, 2018, which is an index prepared by Crisil to measure the extent of financial inclusion in India across 666 districts. While 2 districts i.e. Shravasti, Uttar Pradesh and Malkangiri, Odisha were chosen from the bottom 50 of the Crisil Inclusix 2018, the other 2 districts i.e. Rupnagar, Punjab and Shimoga, Karnataka were chosen from the top 50 of the Crisil Inclusix 2018.

Women respondents from socio-economically weaker areas in particular were chosen given that the PMGKY cash transfers were specifically targeted towards the benefit of low-income PMJDY women account holders. The Study also relied on available data released by government sources and international organisations and existing literature on related issues.

Key findings

- Less than half the women surveyed received the cash transfers for all three months. The Study found that 83% of the total women respondents owned a PMJDY account. Only 23% of such women respondents with PMJDY accounts had received the cash transfer for all three months. Notably, 42% of the women respondents with PMJDY accounts did not receive cash transfer in either of the three months.

- More than 90% women withdrew the cash for regular use. 94% of the women respondents who received the cash transfer in any or all of the three months withdrew the money. Only a small fraction of such women respondents saved the cash transfer (11%) or made online payments (8%) or invested the sum received (3%). Majority of the BC as well as FI respondents indicated that PMJDY account usage post the cash transfer was limited mainly to withdrawals.

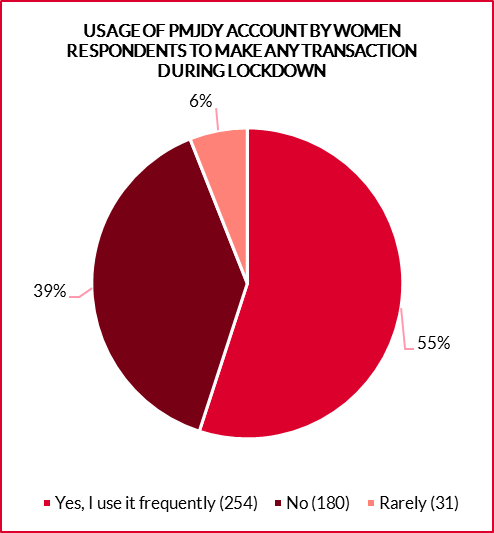

- Use of PMJDY accounts was limited during the lockdown. 45% of the women respondents with PMJDY accounts indicated that they did not use their PMJDY accounts frequently during the lockdown.

- Deposits and overdraft facilities remained under used during the pandemic. The Study sought to understand how women used their PMJDY accounts during the pandemic beyond mere withdrawals. In response to whether the women respondents with PMJDY accounts used deposit and overdraft facility associated with PMJDY accounts during the lockdown and generally during the pandemic respectively, the majority of such women respondents stated that they did not use their PMJDY accounts for deposits (68%) or overdraft facilities (85%).

- Bank branches were preferred sites for withdrawal of money. Women respondents who received the PMGKY cash transfer preferred going to bank branches to withdraw the money in comparison to accessing ATMs, using the services of BCs, or net-banking.

- Lack of supporting infrastructure made access to cash difficult. The main challenges identified by women respondents in accessing banking infrastructure during the lockdown included long travel and cost to avail banking infrastructure, absence of cash in ATMs, BCs not operating, and bank branches not working.

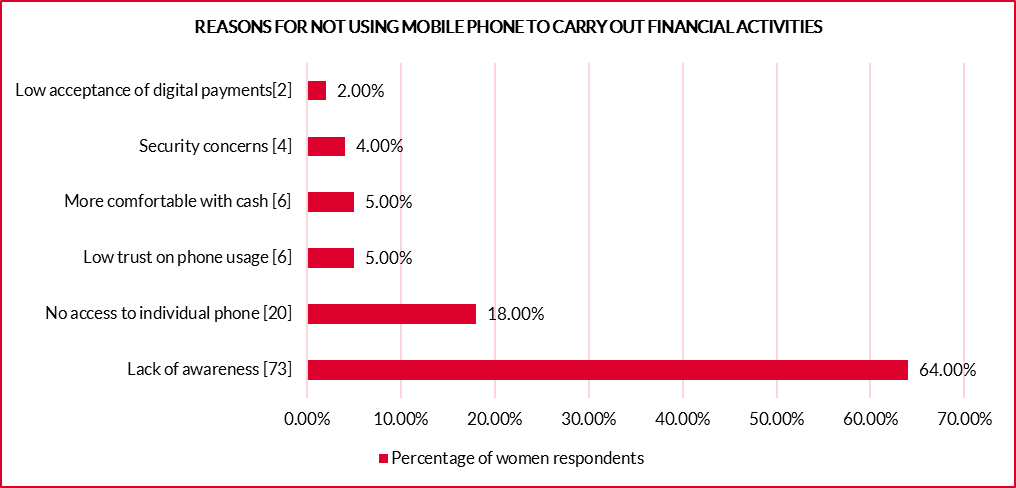

- Very limited use of digital financial services by women. 53% of the women respondents with PMJDY accounts had access to a phone individually and 10% of women respondents with PMJDY accounts had a phone that they shared with others. The financial services undertaken on phones by women respondents were primarily basic financial activities such as checking account balance and receiving account-related notifications. Very few of them undertook advanced digital financial transactions such as online payments or fund transfers.

- Lack of targeted awareness programmes. Targeted communication/awareness programmes on behalf of FIs during the pandemic were largely missing as indicated by the women respondents. Out of the women respondents that indicated awareness campaigns to have taken place, 85% found such campaigns to be useful. Moreover, as indicated by FIs themselves, women-centric financial products were hardly developed and offered to women customers.

- Women preferred female business correspondents. More than 50% FIs suggested that women customers responded better and felt more comfortable using financial services when being served by female BCs.

Way forward

While the PMGKY cash transfer is a step in the right direction to respond to the economic impact of the pandemic, the findings of the Study indicate areas for improvement in order to deal with such emergencies more efficiently in the future. The Study identified the following areas where further policy action is warranted:

Ensuring effective implementation: The findings from the study indicated that there were several women beneficiaries who did not receive the cash transfers for all the three months, raising concerns about the overall implementation of the scheme. Data from existing literature also highlighted how the cash transfer may have been inadequate to compensate for the loss of income during the pandemic. It is possible that the inadequacy of the amount of the cash transfer provided under PMGKY coupled with its non-crediting for all of the three months, may have been the reasons for withdrawals being the prominent financial activity undertaken by majority of the women respondents as opposed to other financial activities such as investments or deposits.

The Government may consider different measures to confirm that all beneficiaries have received the cash transfer for the intended period. This may include making phone calls through designated centers to intended recipients to monitor the implementation of such cash transfers, leveraging the BC network to undertake door-to-door services to confirm receipt and assist beneficiaries in case of any challenges and setting up of online/offline grievance redressal channels wherein beneficiaries can lodge complaints in case of non-receipt. The Government may also consider undertaking an economic impact assessment to assess the impact of events like the pandemic on the income of vulnerable groups of citizens to determine the adequacy of the amount of the cash transfer.

Training and deploying female business correspondents: As indicated by FIs, women customers feel higher levels of comfort with female BCs. There is lesser hesitancy in approaching BCs, which FIs suggested have a better understanding of issues and concerns about women customers. Targeted efforts must be made to equip BCs with appropriate skills to serve women customers, especially women-owned businesses, which the Study noted was missing. Gender-specific training for BCs is important to increase the uptake of more financial products and services by women customers. Moreover, deployment of more female BCs can play a critical role in furthering the financial inclusion of women.

Designing women centric financial services and products: The Study found that the majority of FIs recognised that women have different needs and considerations in availing financial services and products. Therefore, more research should be conducted by FIs on the business case of women-centric products. This is important as findings from the Study indicated that such products were not developed or offered by the majority of the FIs to lower-middle income group women customers during the lockdown.

Promoting the use of digital financial services among women: The findings from the Study indicated that despite having access to a phone, the women respondents either did not use it for financial transactions and the ones who did carry out some financial transactions using their phone, mainly limited its usage to basic financial activities such as checking account balance. Therefore, it is recommended that targeted programmes must be designed to promote the use of digital financial services by women. However, given the high gender digital divide in India, the presence of physical touchpoints should also be bolstered through which women can undertake financial services and get training on how to use digital financial services.

Filed Under

About the Authors

Swarna was a Research Fellow at Vidhi working in the area of Fintech. She graduated from West Bengal National University of Juridical Sciences, Kolkata with a B.A. LL.B (Hons.) in 2021. Her areas of interests include financial regulations, data protection laws, commercial laws and the emerging frameworks of new financial technologies. She previously worked with the law firm L&L Partners wherein she was involved in advising on various issues under the Companies Act, foreign exchange laws and employment laws. She has also worked with the Vidhi Kautilya Society, NUJS and has contributed to the NUJS Law Review.

Manvi Khanna was a Research Fellow in the Law, Finance and Development Team at Vidhi. She completed her BBA.LLB (Hons) from National Law University Odisha, Cuttack in 2021 and is a University gold medallist for highest grades in Corporate and Insurance Laws. Prior to joining Vidhi, she had interned in the commercial disputes team at J Sagar Associates, New Delhi, project finance team at L&L Partners, New Delhi, disputes team at Shardul Amarchand Mangaldas, New Delhi, LKS, New Delhi and Bharucha and Partners, New Delhi. Throughout her law program she has authored numerous research pieces in the form of opinion editorials, blogs and journal articles. She has also been a member of the Centre for Corporate Law, Legal Aid Society and Centre for Women and Law at college. Her areas of interest include finance, insolvency, banking and gender justice.

Shreya was a Senior Resident Fellow, and lead the work at the intersection of law, finance and development at Vidhi. She focused on independent research work relating to financial inclusion, tech and corporate governance. She has worked on several engaged projects with the International Financial Services Centres Authority, Ministry of Corporate Affairs and the Insolvency and Bankruptcy Board of India. Shreya completed her LLB from National Law University, Jodhpur in 2012 and LLM from Queen Mary, London on a Chevening scholarship in 2019. She also worked with the European Bank for Reconstruction and Development, London in 2019. Prior to joining Vidhi in 2014, she worked as an Associate at Luthra & Luthra Law Offices, New Delhi.

Shehnaz leads the Applied Law and Technology Research (ALTR) at Vidhi, where she specialises in technology law and policy. At Vidhi, she has worked with several Government Ministries/ Departments and regulators on matters relating to digital public infrastructure, data protection, artificial intelligence, and fintech. Her work at Vidhi focuses on developing legal and policy solutions to ensure that innovation serves society equitably and responsibly. Before joining Vidhi, she also worked with the Financial Regulatory Practice at Cyril Amarchand Mangaldas.