Blueprint of a Law for Regulating Cryptoassets

Over the past few years, cryptoassets have seen an exponential rise in its usage and adoption. As per the International Monetary Fund, there has been a ten-fold increase in the market value of cryptoassets since early 2020 with the value surpassing USD 2 trillion as of September 2021. While proponents of cryptoassets argue about the innovation potential of cryptoassets and its underlying technology (i.e. blockchain) for the financial system, this rise in cryptoassets along with its volatility has raised concerns about its risks to investors and the financial system. Therefore, designing an appropriate cryptoasset regulation has become a subject of intense policy debate.

While India’s initial policy response was towards a ban on dealing with such cryptoassets, policy direction (based on statements by government officials) now appears to be moving towards regulating cryptoassets. While the Cryptocurrency and Regulation of Official Digital Currency Bill, 2021 was sought to be introduced in the last two sessions of the Parliament, there is no clarity on the contours of the proposed law. As India continues to debate and deliberate on the nuances of the regulatory approach to cryptoassets, this report presents a blueprint of a standalone law to regulate cryptoassets in India that will promote responsible innovation in the crypto economy as well as counter the associated risks.

Understanding Key Concepts

This Report analyses certain key terms that are necessary to be understood for understanding the various regulatory frameworks:

- Cryptoassets: It may be broadly defined as a digital representation of value or right issued by a private entity and that relies on cryptography, distributed ledger technology or similar technology as a part of its inherent value. [See definition provided by the Financial Stability Board] (“FSB”)]. Bitcoin (BTC) and Ether (ETH) are two of the most popular cryptoassets.

- Stablecoins: It is a type of cryptoasset that seeks to maintain a stable value. This may be achieved by pegging its value to asset(s) such as a single fiat currency, basket of currencies or commodities or other cryptoassets. Tether (USDT) is one of the most popular stablecoins. [See definition provided by the FSB]

- Distributed Ledger Technology (“DLT”): DLT is the underlying technology of cryptoassets. It refers to processes and related technologies that enable participants (nodes) in a network to securely propose, validate and record changes to a ledger that is distributed across the network’s participants. [See definition provided by Bank for International Settlements]. It does not rely on a centralized controller. Depending of their design and architecture, DLT systems maybe of different types. Blockchain (that is the underlying technology of the popular cryptoasset Bitcoin) is a type of DLT which is based on verifying and adding transactions on a block.

Classification of Cryptoassets

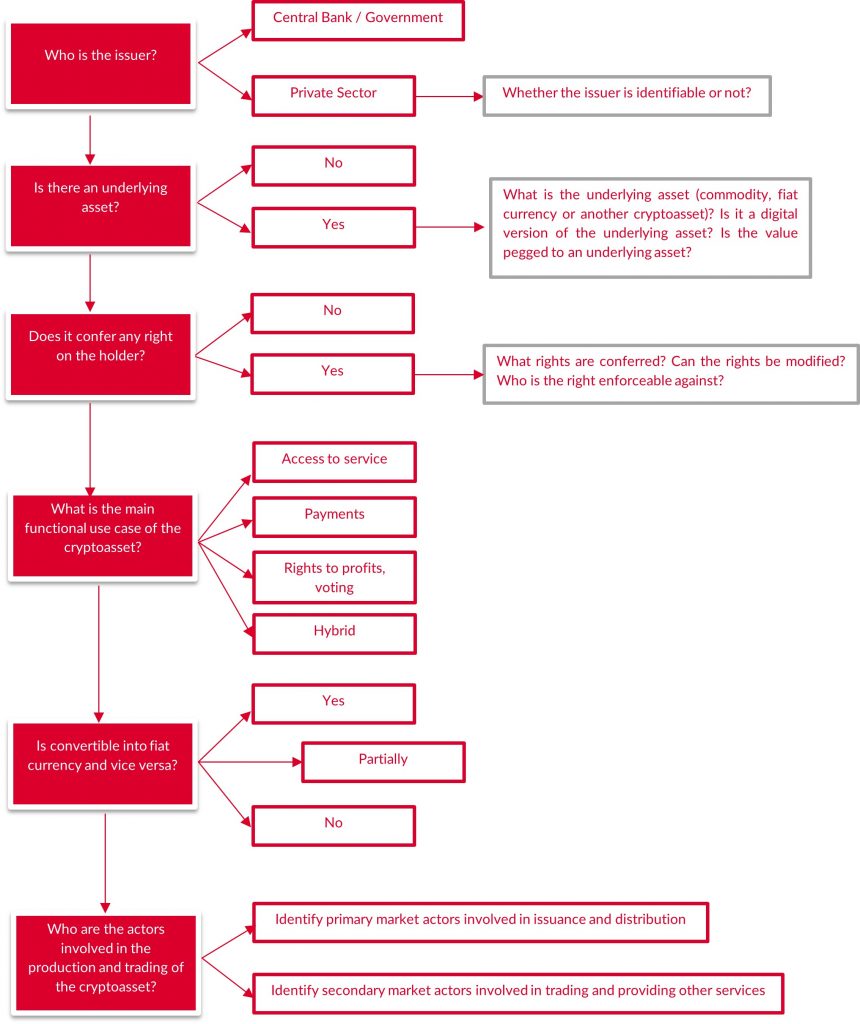

The Report recognizes the challenges in compartmentalizing cryptoassets into one single category. It analyses how different parameters such as nature of issuer, method of production, manner of transfer/trading etc. may affect the classification of cryptoassets and therefore, the regulatory contours. In this context, the Report identifies the following key questions/issues that must be considered by policymakers to assess the key features of cryptoassets which in turn will be instrumental in designing the legal and policy framework for cryptoassets:

Global Regulatory Approaches

Across the globe, the regulatory response to cryptoassets has been varied. While there are countries such as China that has banned the use of cryptoassets, there is El Salvador which has recognized bitcoin as a legal tender. However, predominantly a balanced approach has been undertaken by most jurisdictions. This approach towards regulation has been categorised under three groups in the Report:

- Reliance on existing laws: Regulators rely on existing laws (mostly securities law) to clarify its applicability to certain types of cryptoassets, primarily security tokens issued during an initial coin offering. Notable examples include clarifications issued by the US Securities and Exchange Commission in 2019 and Australian Securities and Investment Commission in 2021.

- Amendment to existing laws: Regulators amend existing laws (mostly anti-money laundering laws) to bring cryptoasset related services within its ambit. A notable example is South Korea’s amendment to the Act on Reporting and Using Specified Financial Transaction Information Act 2001 in 2021. The amendment defines “virtual assets” and brings “virtual asset providers” within the ambit of the law.

- Enacting a Standalone Law: A new standalone law is enacted to regulate cryptoasets. In 2021, the Council of European Union adopted its position on the draft Regulation on Markets in Crypto Assets (“MiCA”) – a framework governing issuance and provisions of cryptoasset related services. This will mark the beginning of negotiations on MiCA with the EU Parliament. Previously, Malta and Thailand have also enacted standalone frameworks for cryptoassets in 2018.

Some countries are also adopting a phased approach in regulation wherein they are focusing on regulating cryptoassets that are presently the dominant use case in such jurisdictions. Specifically, jurisdictions such as Hong Kong, the United States of America and the United Kingdom are focussing on developing regulations for stablecoins which is the prevalent use case presently in such countries.

Recommendations | A Blueprint of a Law to Regulate Cryptoassets

This Report examines how regulation over banning would be more effective in addressing the issues posed by cryptoassets. In regulating cryptoassets, the Report analyses two approaches: (a) reliance on existing laws to regulate the cryptoasset sector; and (b) enacting a standalone law. On the basis of this analysis, the Report recommends that the most viable and effective solution would be to formulate a standalone law to regulate cryptoassets. The key recommendations of the Report are set out below:

- Enact a standalone law to regulate cryptoassets in India known as the “Regulation of the Cryptoasset Market Act” (Proposed Law).

- The Proposed Law should regulate issuers of cryptoassets and entities providing cryptoasset related services as defined under the law.

- The framework may distinguish between asset-backed / fiat currency-backed cryptoassets popularly referred to as ‘stablecoins’ and other types of cryptoassets. RBI will be responsible for regulating the former category of cryptoassets and SEBI will be responsible for the latter category.

- SEBI will be responsible to regulate cryptoasset service providers.

- RBI will also be empowered to designate significant cryptoassets and significant cryptoasset service providers that may pose systemic risks. Once designated, such cryptoassets and service providers will be subject to stringent oversight of RBI.

- Issuer of asset backed / fiat backed cryptoassets will be subject to authorisation requirement along with the requirement to file prospectus / whitepaper for issuing cryptoassets in India and for admission to trading on a trading platform. Issuers of other cryptoassets will only be subject to requirement to file prospectus / white paper with concerned regulator (SEBI). The Proposed Law also sets out other specific requirements that must be complied with by such issuers, more specifically issuers of asset backed / fiat backed cryptoassets.

- Cryptoasset service providers will be required to obtain an authorisation from SEBI to provide services. They will also be subject to requirements relating to communications with investors, customer due diligence, investor protection, prevention of market abuse, etc.

- The Proposed Law also empowers the Central Government (in consultation with Reserve Bank of India (“RBI”) and Securities and Exchange Board of India (“SEBI”)) to notify a list of “Prohibited Cryptoassets” and also prohibit / restrict specific use cases of permissible cryptoassets

- The Proposed Law also envisaged the creation of an Inter-Regulatory Council consisting of representatives of Ministry of Finance, RBI and SEBI.

- It also contemplates setting up of a self-regulatory organisation of cryptoasset service providers to focus on issues such as cyber security.

Along with the Proposed Law, India must also focus on investment in creating a specialised taskforce consisting of skilled officers for enforcing the provisions of the law, investment in investor education and also fostering partnerships with other countries for effectively regulating cryptoassets.

Consultation Update: To inform the research and the key recommendations of Vidhi’s Working Paper on ‘Blueprint of a Law for Regulating Cryptoassets’, consultations were organised from April to June 2022 with stakeholders from the industry, academia, research and law. The key takeaways from the consultations can be accessed below.

Filed Under

About the Authors

Shehnaz leads the Applied Law and Technology Research (ALTR) at Vidhi, where she specialises in technology law and policy. At Vidhi, she has worked with several Government Ministries/ Departments and regulators on matters relating to digital public infrastructure, data protection, artificial intelligence, and fintech. Her work at Vidhi focuses on developing legal and policy solutions to ensure that innovation serves society equitably and responsibly. Before joining Vidhi, she also worked with the Financial Regulatory Practice at Cyril Amarchand Mangaldas.

Swarna was a Research Fellow at Vidhi working in the area of Fintech. She graduated from West Bengal National University of Juridical Sciences, Kolkata with a B.A. LL.B (Hons.) in 2021. Her areas of interests include financial regulations, data protection laws, commercial laws and the emerging frameworks of new financial technologies. She previously worked with the law firm L&L Partners wherein she was involved in advising on various issues under the Companies Act, foreign exchange laws and employment laws. She has also worked with the Vidhi Kautilya Society, NUJS and has contributed to the NUJS Law Review.