Halting Tribunalisation: Impact of the Judgment of the Supreme Court of India in Madras Bar Association v Union of India on Extant Tribunals

Judicial impact assessment on tribunal framework in India

Summary: The report studies the Madras Bar Association v Union of India judgment and analyses its impact on the functioning of tribunals.

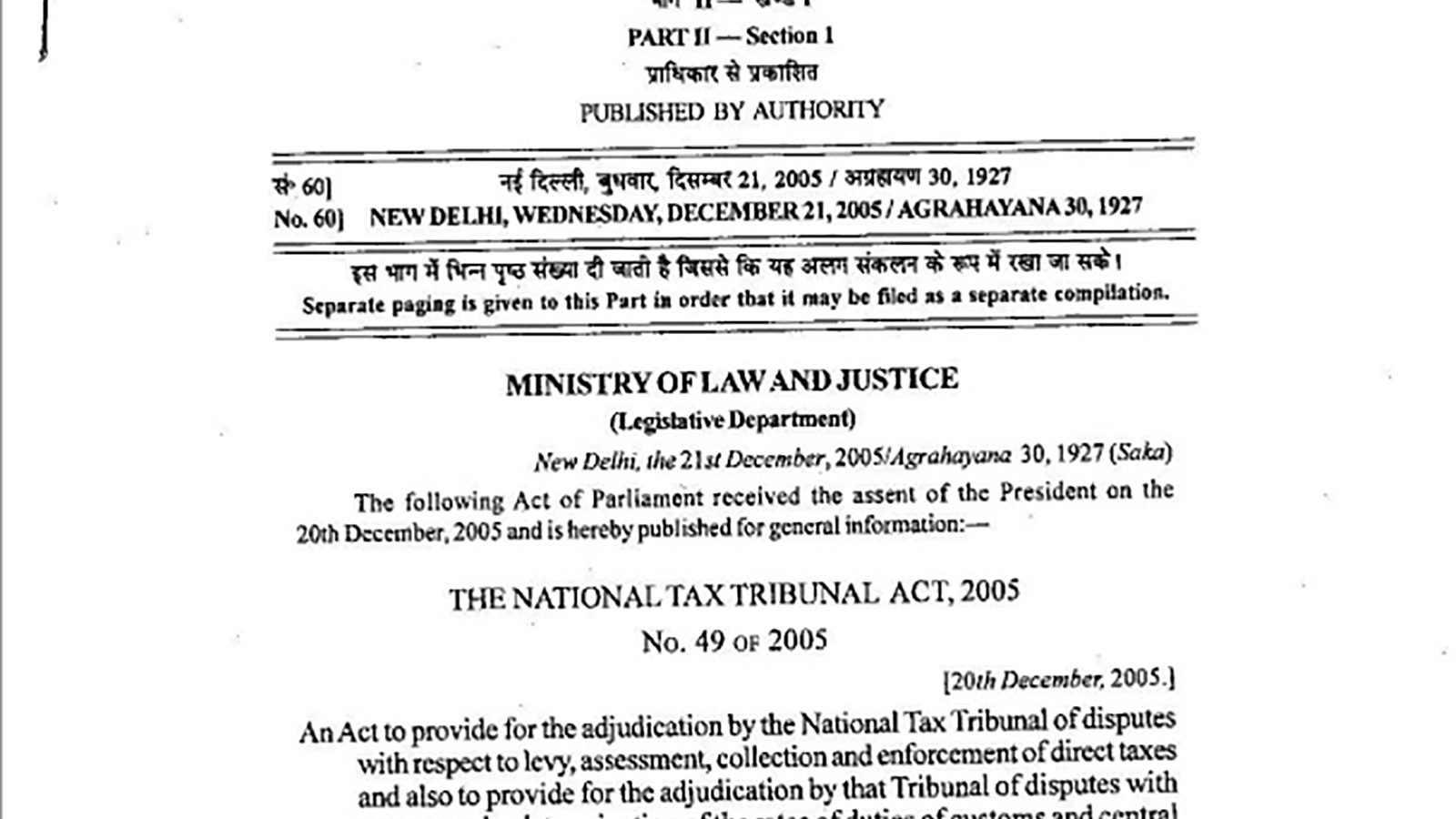

On the 25th of September, 2014, a Constitution Bench of the Supreme Court of India struck down the National Tax Tribunals Act, 2005 (“NTT Act”) in its judgment in Madras Bar Association v Union of India1 (hereinafter “NTT case”). The National Tax Tribunal (“NTT”) was set up to take over the existing jurisdiction of High Courts in India to hear and decide appeals pertaining to ‘questions of law’ relating to Income Tax, Customs, Central Excise and Service Tax matters, arising from the Income Tax Appellate Tribunal and the Customs, Excise and Service Tax Appellate Tribunal.

To understand the impact of the NTT judgment on individual tribunals, this note will analyse the parameters laid down by the Supreme Court in the NTT case in examining the provisions of the NTT Act and see how the same parameters could be applied to the provisions of other tribunal legislation. This exercise will point out where the defects in existing tribunal legislation and how they may be fixed to ensure constitutional compliance on the basis of the judgment in the NTT case.

Filed Under

About the Authors

Alok Prasanna Kumar is Co-Founder and Lead, Vidhi Karnataka. His areas of research include judicial reforms, Constitutional law, urban development, and law and technology. He graduated with a B.A. LL.B. (Hons) from the NALSAR University in 2008 and obtained the BCL from the University of Oxford in 2009. He writes a monthly column for the Economic and Political Weekly and has published in the Indian Journal of Constitutional Law and National Law School of India Review apart from media outlets such as The Hindu, Indian Express, Scroll, Quint and Caravan. He has practiced in the Supreme Court and Delhi High Court from the chambers of Mr Mohan Parasaran, and currently also co-hosts the Ganatantra podcast on IVM Podcasts.